Latin America's Mega Series A Rounds: Pattern or Anomaly?

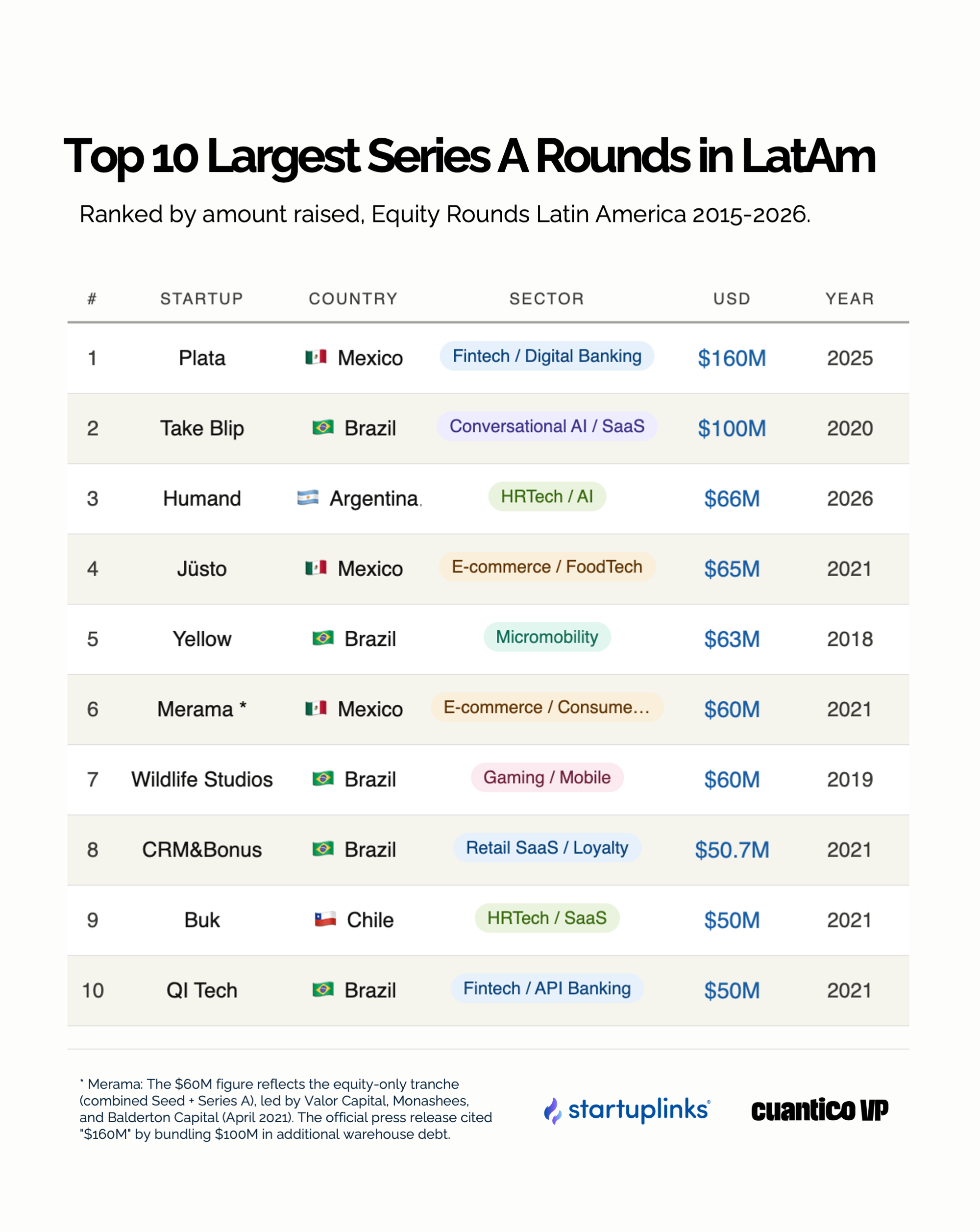

In ten years, only ten Series A rounds have crossed the $50 million threshold in the region. Each tells a different story about where the ecosystem stands and where it's headed.

When Plata, the Mexican fintech founded by three former executives of Russian digital bank Tinkoff, closed a $160 million Series A in March 2025, headlines celebrated the new regional record. And rightly so: the round more than doubled the previous all-time high and turned the company into a unicorn overnight, at a $1.5 billion valuation. But the more interesting story isn't in that isolated number. It's in what it reveals when placed alongside the other nine largest rounds that Latin American venture capital has produced in a decade.

After analyzing and cross-checking primary coverage records of each transaction, the picture that emerges is more complex and more fascinating than any celebratory headline.

A 13-Month Window That Explains Almost Everything

The most striking fact in the ranking isn't who's in it. It's when they arrived.

Seven of the ten largest Series A rounds in Latin American venture history closed in a period of just 13 months, between October 2020 and November 2021. Warburg Pincus opened the season with Blip ($100M). General Atlantic set the ceiling with Jüsto's Series A ($65M). And then, in a span of just five weeks between October and November of that same year, came Buk, CRM&Bonus, and QI Tech—all three at $50 million.

It wasn't that the ecosystem matured overnight. Interest rates were at historic lows, global liquidity was seeking returns, and funds like SoftBank, Tiger Global, and GGV were deploying capital at a speed the region had never seen. When the FED began normalizing rates in 2022, the pace moderated just as quickly. Between 2022 and 2024, no Latin American Series A crossed $50 million.

That pattern doesn't invalidate what was built during those months—many of the companies from that generation are still operating and generating real value. But it does invite a more honest reading: part of the boom reflected exceptional global macroeconomic conditions, and understanding that helps better calibrate what's coming.

According to Jose Kont, CEO of Cuantico VP, "The 2021 boom was not a cycle but a statistical anomaly that revealed our region's dependence on foreign capital. What's important to note is that this wasn't unique to Latin America—it happened globally, and the lessons learned have allowed the industry to develop greater discipline today."

Mexico and Brazil at the Forefront

Brazil contributes five companies to the ranking. Mexico, three. Chile appears with Buk. Argentina debuts in 2026 with Humand. Colombia, Peru, Uruguay and Central America still have no representation on this list.

The concentration along the Brazil-Mexico axis is no surprise: both markets combine population size, financial infrastructure, strong technical universities, and a critical mass of local venture capital that facilitates large rounds. São Paulo and Mexico City have the deal flow, senior talent, and legal and accounting ecosystems that make these transactions possible.

What's interesting is that the rest of the region is building that same scaffolding at an accelerated pace. Bogotá, Lima, Santiago, and San José are producing more and more startups with regional traction, and global funds are beginning to pay them more serious attention. That Argentina appears in the top 10 with Humand in 2026—a company founded in Buenos Aires with clients in 51 countries—is a signal that Latin American venture geography is expanding.

Plata Rewriting the Rules of the Game

Until March 2025, the region's largest Series A was Jüsto at $65 million. Plata arrived with $160 million—two and a half times that ceiling—and did so in a way that deserves careful examination.

Before its first equity round, Plata had quietly built a $590 million debt base with Nomura and Fasanara and had obtained a banking license from the CNBV in December 2024. It didn't arrive as a startup seeking product-market fit: it arrived as a fully regulated digital bank, with credit infrastructure already deployed and operating metrics of a company in full growth mode.

That pattern—build first with debt, raise equity later—could become the new playbook for high-growth Latin American fintech. If so, the traditional concept of "Series A" in the region is being redefined from within: less bet on the future, more validation of an already-working model. For investors, that's good news.

AI Gaining Ground

Humand ($66 million, February 2026) is the first company in the top 10 whose core product is artificial intelligence—not as an additional feature, but as business architecture. The Argentine startup created a platform to digitize operational workers without computer access: employees at OXXO, Domino's, and MINISO, factory workers, hospital and hotel staff who represent nearly 80% of the global workforce but for whom traditional enterprise software was never designed.

What's most revealing isn't the amount. It's the cap table: Kaszek, Goodwater Capital, and some of the founders of Dropbox, Rappi, Lyft and Mercado Libre. That group doesn't back generic trends—they back categories they believe will define the next cycle. The fact that Humand reached its Series A with 1.6 million users in 51 countries and regional-scale clients suggests that the moment for large AI rounds in Latin America isn't on the horizon. It's already begun.

The Real Pattern Isn't Fintech, It's Something Deeper

Viewed superficially, the ranking seems dominated by fintech: Plata, CRM&Bonus, and QI Tech account for three of the ten spots. But if you look at what concrete problem each company solves, a more precise pattern emerges.

They all attack the same gap: the distance between how people and companies operate in Latin America and the digital infrastructure standards of the developed world. Humand digitalizes workers who never had corporate email. QI Tech gives banking infrastructure to companies the traditional financial system didn't serve. Blip connects businesses with customers on WhatsApp because that's always been the real communication channel in the region, not email. Wildlife Studios built mobile-first games because PC gaming never penetrated markets where the smartphone was the first—and often only—digital access device.

The sector isn't fintech, nor HRtech, nor gaming. It's the digitization of an economy that jumped straight to mobile without passing through desktop. The companies that understood that before anyone else are the ones appearing on this list.

The Next Chapter: Converting Paper Value into Real Returns

Of the active companies in the ranking, four hold unicorn status (Plata, Wildlife, Merama, QI Tech) and two others have significant valuations (Buk, Humand). The ecosystem, viewed from that lens, has much to be proud of.

The coming challenge is of a different nature. The Latin American exit market—exits via IPO, strategic acquisition, or secondary—remains the weakest link in the ecosystem. The funds that backed these rounds have committed capital in assets that generate real value, but whose liquidation requires paths that are still being built: deeper regional public markets, more strategic buyers with appetite for Latin American assets, and a more active M&A culture among the ecosystem's own leaders.

That is, probably, the most important chapter left to be written by Latin American venture capital. And judging by the speed at which the region is moving—Plata as a regulated bank in its Series A, Humand with presence in 51 countries before raising its first growth round, QI Tech becoming a unicorn four years after its Series A—there are solid reasons for optimism.

The map is being redrawn. And the most interesting part is yet to come.