Central America and the Caribbean: the frontier GPs and LPs are not looking at

Central America today is what Mexico and Chile were ten years ago for venture capital: a market that does not appear in any LP’s deck — but should.

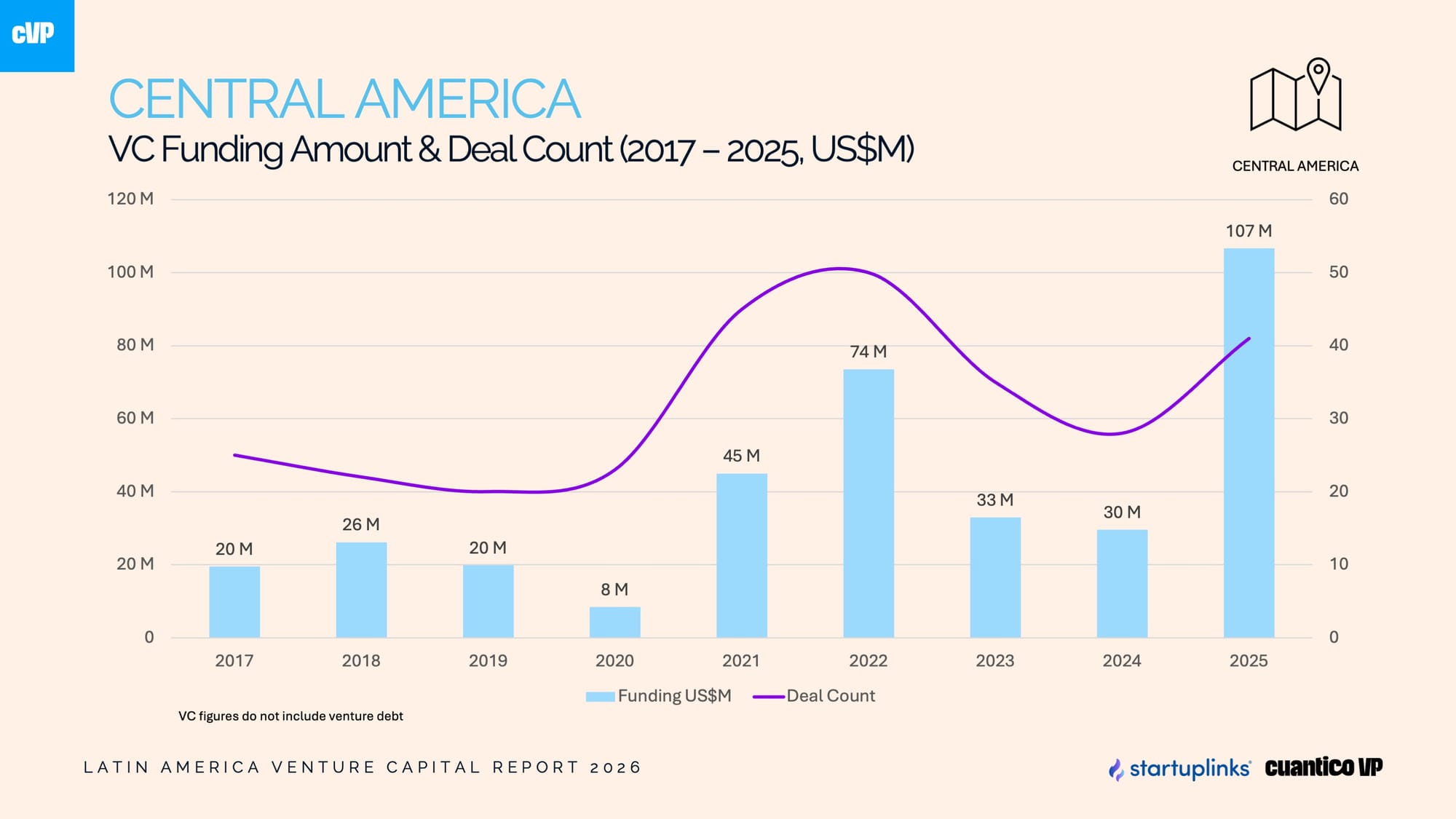

In 2025, the region captured US$107 million across 41 rounds, just 2.6% of Latin America’s total VC. Yet that is 5 times what was invested five years earlier. There are startups billing millions of dollars, funds backed by the IFC and IDB, companies from the region with Y Combinator on the cap table, and a diaspora of more than 7 million Central Americans in the U.S. sending US$45.7 billion in remittances every year, more than the GDP of many countries in the region.

But talking about “Central America” as a homogeneous bloc is a mistake. Each country is a completely different reality. To understand it, the region must be viewed in four blocs.

The Caribbean: lots of tax incentives, little VC

The Caribbean mixes jurisdictions with world‑class incentives like Puerto Rico and the Cayman Islands with markets where venture capital is practically nonexistent.

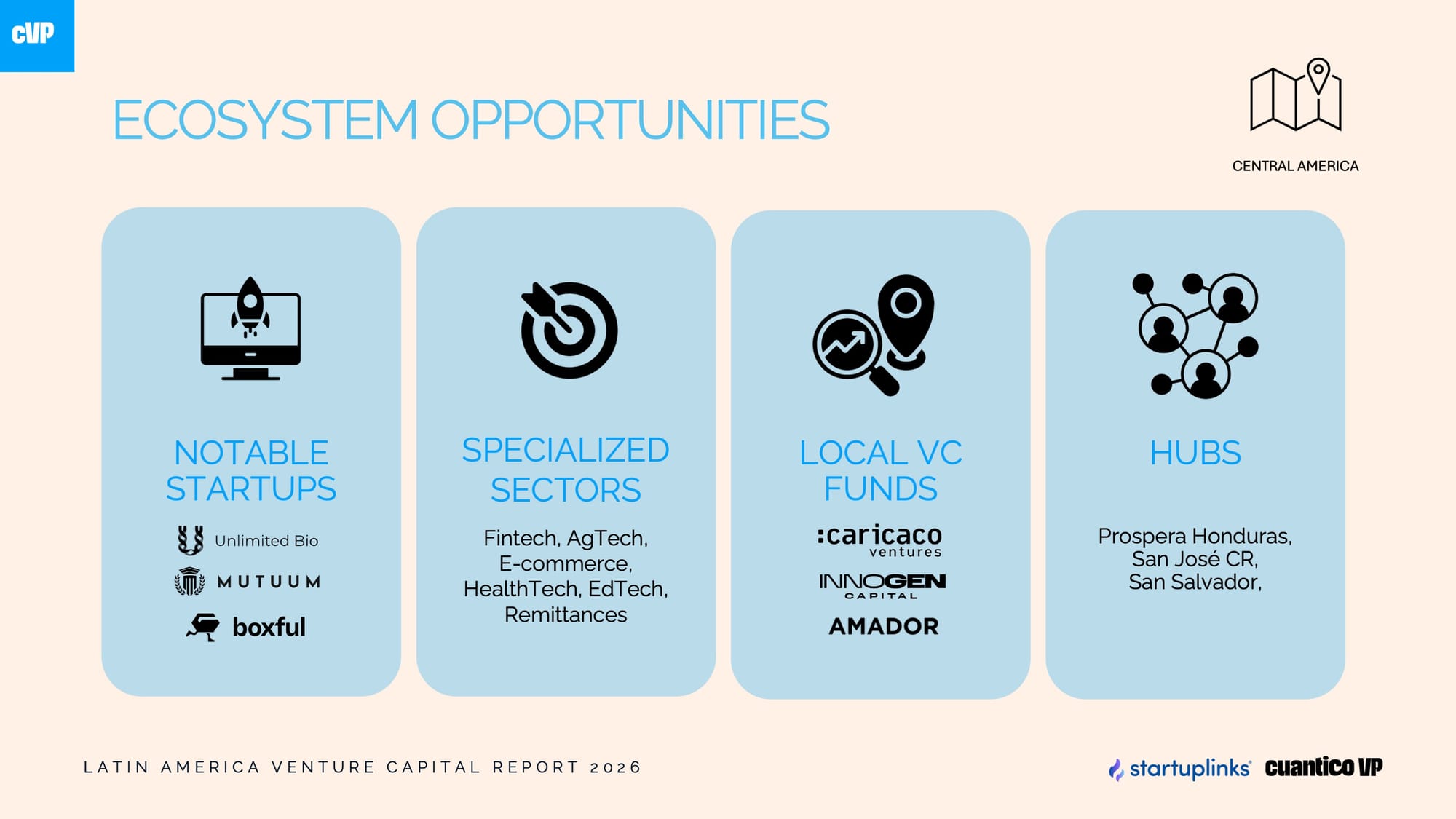

- Puerto Rico is by far the leader. Act 60 offers a 4% corporate tax rate for exported services, full exemption on dividends and (until recently) 0% tax on capital gains. More than 4,000 investors operate under this framework. San Juan has become a crypto hub with 17 blockchain startups. Morro Ventures raised US$17 million for its first fund focused on pre‑seed and Series A. And Parallel18, the government accelerator, has supported more than 302 companies with a cumulative portfolio valuation of US$847 million — not bad at all for a Caribbean island.

- The Dominican Republic is surprising, with 923 registered startups according to Tracxn and a significant increase in funding rounds since 2023. Venture Do operates as an early‑stage fund out of Santo Domingo, and the IDB financed a US$1.5 million project to accelerate the Dominican VC ecosystem.

- Jamaica has the number‑one startup ecosystem in the Caribbean according to StartupBlink, and the Caribbean Venture Capital Fund — a US$50 million fund backed, among others, by musician Burna Boy — is the largest in the sub‑region.

- Cuba remains essentially closed to venture capital: MSMEs were only legalized in July 2022 and 125 economic activities are still prohibited.

- Haiti shows resilience with local incubators such as ANTREPRANN but faces insurmountable structural challenges.

- The Cayman Islands host 111 VC funds as a domicile jurisdiction according to Tracxn, but they have no relationship with the local ecosystem.

The Northern Triangle: three countries, three radically different bets

Guatemala, El Salvador, and Honduras share geographic proximity and socioeconomic challenges, but their strategies to attract venture capital are completely different. Guatemala is betting on social‑impact entrepreneurship from the ground up. El Salvador has built the most attractive fiscal framework in the Western Hemisphere for tech companies, and Honduras, through Próspera, has created an unprecedented regulatory sandbox that has attracted investors such as Peter Thiel and Marc Andreessen.

- Guatemala is the most populous country in Central America with 20 million inhabitants — and the least developed in high‑impact entrepreneurship (startups). Not a single university teaches what a startup is or how venture capital works. The exception is Universidad del Valle, which, thanks to its emphasis on science and mathematics, has produced some of the few tech founders in the country. Guatemala’s most funded startup, Osigu (US$52.3 million raised, including investment from Visa), operates out of Florida — the classic talent flight pattern. One of the relevant ecosystem players is CAFI, the first angel investment network in all of Central America, which together with Startuplinks and other partners created the region’s first venture capital diploma program (FUVECA). Guatemala has all the demographic potential (a median age of 23.8 years, the youngest in the hemisphere), but it lacks the institutional infrastructure to capitalize on it.

- El Salvador is the opposite story: a country that decided to compete purely through fiscal policy. The Innovation Promotion Law grants a full tax exemption for 15 years to software, AI, blockchain, cybersecurity, and quantum computing companies. Zero income tax, zero capital gains tax on Bitcoin, zero municipal taxes. Tether relocated its headquarters there in January 2025. In fact, Hugo App, the first Central American super‑app with more than 500 employees operating in 6 countries, is the region’s most visible case study. Impact Hub and Innogen Capital’s Delta Fund 1 aims to invest US$10 million in 18 startups. And the dollarization of the economy eliminates FX risk, an advantage international investors do not underestimate.

- Honduras is the most polarizing case. Próspera, the special zone (ZEDE) in Roatán founded by Venezuelan‑American Erick Brimen, operates with its own commercial code, allows companies to choose regulations from OECD jurisdictions, and charges just 1% on gross revenue (versus the standard 25% in Honduras). The list of investors who have backed this Honduran hub is straight out of science fiction: Peter Thiel, Marc Andreessen, Sam Altman, Balaji Srinivasan, and more recently Brian Armstrong from Coinbase. More than 300 companies are incorporated there, including Minicircle, a gene‑therapy startup that launched clinical trials at a fraction of the cost and time it would take in the U.S. But the political risk is existential: President Xiomara Castro repealed the ZEDEs, the Supreme Court declared them unconstitutional, and Honduras Próspera Inc. sued the country for US$10.775 billion at ICSID. As of March 2026, it continues operating while the legal battle unfolds. According to the Latin America VC Report published this year, Central America’s VC investment peak in 2025 is largely explained by what is happening in Próspera Honduras.

Costa Rica and Panama: the Central America that already works

If the Northern Triangle is a zone of contrasts and opportunities, Costa Rica and Panama are the polished version of Central America. With GDP per capita of US$14,867 and US$17,137 respectively, 92% internet penetration, and professional institutional ecosystems, both countries present a different reality that does not go unnoticed by GPs and LPs.

- Costa Rica is the most mature VC hub in the region. Carao Ventures raised US$35 million for its Fund I — the IFC’s (World Bank) first investment in Central America — and has invested in more than 35 companies with co‑investors such as Y Combinator, 500 Global, and IGNIA. Caricaco Ventures is a firm whose thesis focuses on Central America and invests between US$100K and US$5M. At its annual Caricaco Summit, it has attracted top‑tier regional investors such as Endeavor Catalyst and Monashees. Perhaps what not many know is the ace up Costa Rica’s sleeve: CINDE, the country’s investment promotion agency, considered the most effective in the world for five consecutive years according to the International Trade Center. It has guided more than 450 multinationals into the country, including 29 from the Fortune 100. Microsoft opened its largest Latin American office in Costa Rica. Intel, Amazon, HP, IBM, and Akamai all have substantial operations. CINDE has an active presence in Silicon Valley — participating in events such as SEMICON West in San Francisco and maintaining offices in New York. Costa Rica was chosen as a strategic partner of the CHIPS Act for semiconductors in the Americas. Its nickname says it all: the “Silicon Jungle.”

- Panama complements this with different advantages. A dollarized economy from day one, the largest banking center in Latin America with more than 80 banks, and a territorial tax system that only taxes income generated within the country. Panama Pacifico, the special zone on the former Howard Air Base, is home to more than 365 companies including Dell, 3M, and P&G. And Tesorio, co‑founded by Panamanian Carlos Vega, is an example of the type of startups the ecosystem produces; it has raised more than US$30 million from Y Combinator and First Round Capital and serves clients such as Slack, Twilio, GitLab, and Bank of America.

Belize and Nicaragua: the margins

Neither Belize nor Nicaragua has the development conditions of Costa Rica and Panama, nor the critical mass or regulatory dynamism of the Northern Triangle. They represent the extremes of the spectrum: markets where entrepreneurship exists but is fundamentally subsistence‑based or, at best, produces tech SMEs without regional scale.

- Belize, with just 430,000 inhabitants (one of the smallest populations in the hemisphere) and a GDP per capita of US$6,623, has only 4 startups tracked by StartupBlink. Its English‑speaking status connects it culturally to the Caribbean and North America but isolates it from Spanish‑speaking Central American networks. Internet penetration is around 65%, and 41% of the population lives below the poverty line. The IDB has financed a project to create the country’s first startup community and incubator, and the government allocated US$1.5 million to tech training programs in 2022, but the reality is that the market lacks the minimum critical mass to attract venture capital.

- Nicaragua is the most dramatic case. Under the authoritarian regime of Daniel Ortega and Rosario Murillo, the country has experienced the largest emigration wave in its modern history since the 2018 political crisis, including intellectuals, academics, engineers, and tech professionals. The United States placed Nicaragua in Export Administration Regulations Group D:1 in March 2024, severely restricting technology exports. Correspondent banks have withdrawn (Wells Fargo and Bank of America ended relationships with local banks), and ProNicaragua, the investment promotion agency, was eliminated in 2022 and replaced by a secretariat controlled by Laureano Ortega, the president’s son, who is sanctioned by OFAC. With GDP per capita of just US$2,290, only 5% fixed broadband penetration, and no local venture capital funds, Nicaragua is functionally excluded from the venture capital ecosystem. Dealroom.co explicitly classifies it as a “low VC activity region.” Even so, within this adverse context, two Nicaraguan startups — TuMoni (a remittances digital wallet) and EasyMD (telemedicine) — managed to enter the Top 20 most promising startups in Central America 2026, proving that talent exists even in the most hostile environments.

The big opportunity: US$45 billion looking for a new home

Where is the real opportunity for GPs and LPs? In the numbers no one is connecting.

- More than 7 million Central Americans live in the United States. They send US$45.7 billion in remittances annually — a flow that exceeds the region’s combined foreign direct investment, tourism, and exports. Guatemala alone received US$21.5 billion in 2024, double the 2019 figure.

- Eighty percent goes to consumption. But what would happen if 1% were channeled into investment? One percent of US$45.7 billion is US$457 million — more than all the venture capital Central America captured in 2025. There is not a single firm today dedicated to Central American diaspora capital. That is a first‑mover opportunity.

- The model exists. Israel launched the Yozma funds in 1993 with US$100 million. Before that it had only one active VC fund. Within a decade it had 60, managing US$10 billion. Annual VC investment went from US$58 million to US$3.3 billion — a 57x increase. Today Israel has more than 276 funds and over 70 unicorns.

- Central America does not need to replicate Israel. But it has ingredients Israel did not: the same time zone as the U.S., operating costs 50–80% lower (a developer in Guatemala earns US$14,000–21,000 per year vs. US$132,000 in the U.S.), a young population with a median age of 25–30 years, and a menu of tax incentives that competes with any jurisdiction in the world.

- And Costa Rica has already shown how to execute: CINDE built a direct presence in Silicon Valley and New York. The result: 450 multinationals, 196,000 jobs, and the title of number‑one country in the world for foreign direct investment attraction per capita according to the Financial Times for two consecutive years.

The 20 startups that prove the thesis

The ranking of the 20 most promising startups in Central America, presented at Caricaco Summit 2026 and produced in collaboration with Startuplinks and local funds in the region, is the best evidence that the ecosystem is producing real companies.

Costa Rica and El Salvador lead with 6 startups each. Fintech dominates with 45%. Eighty percent have already received external capital. These are some of the names to know:

- Tesorio (Panama) — US$35M raised, clients such as Slack and Bank of America.

- Huli (Costa Rica) — 7 million patients connected across 5 countries.

- Boxful (El Salvador) — 18% monthly growth, aiming to become Central America’s first unicorn.

- Ábaco (El Salvador) — digital factoring growing 30% month over month.

- TuMoni (Nicaragua) — free remittances between the U.S. and Central America.

- Snap Compliance (Costa Rica) — multi‑jurisdiction automated compliance.

- Sento AI (Guatemala) — winner of CAFI and Google Cloud’s Central America AI Challenge.

What unites these 20 companies is a distinctive trait of Central American innovation: they are born solving local problems with regional ambition from day one. The domestic market of any individual Central American country is too small to sustain a high‑growth startup, which forces founders to think multi‑country from the outset — a mindset that, paradoxically, makes them better prepared for international expansion than founders in large markets like Brazil or Mexico, where the domestic market can delay internationalization.

The full mapping is available here: The 20 Most Promising Startups in Central America, According to Investors in the Region.

According to Jose Kont, “Central America does not need permission to enter the Latin American VC map. It is already on it. What it needs is investors with the vision to see beyond the conventional narrative and the capital to turn the region into Latin America’s next center of gravity for innovation.”

Central America is at a tipping point

The region’s venture capital ecosystem grew 5x in five years, from less than US$20 million per year to US$107 million in 2025. Cumulative investment over the last six years exceeds US$266 million. There are 15 startups with multimillion‑dollar revenues, funds like Carao (US$35M) and Caricaco operating professionally, a regional venture capital association (CAPCA, founded in 2021), and a Central American angel network (CAFI, launched in 2023). Costa Rica was named the number‑one country in the world for foreign direct investment attraction per capita by the Financial Times for the second year in a row. El Salvador offers the most aggressive tech‑focused fiscal policy in the hemisphere, and finally Honduras, with all its controversies, is attracting the attention of some of the most recognized names in global venture capital.

Central America is not a bet for everyone. It is a region with varying levels of risk, evolving regulatory frameworks, and ecosystems still under construction. But that is precisely where the opportunity lies: the markets that seem too early today are the ones that generate the best returns for those who arrive first. The question is no longer whether Central America has potential, the data confirm it. The question is who will have the vision to bet on the ecosystems of the future.